Kapcsolat

Kapcsolat Hogyan vásároljunk

Hogyan vásároljunkKézbesítés

Vásárlási tanácsadó

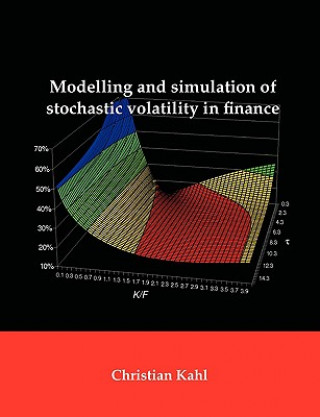

Modelling and Simulation of Stochastic Volatility in Finance

Angol

Angol

79 b

79 b

30 nap a termék visszaküldésére

Ezt is ajánljuk

The famous Black-Scholes model was the starting point of a new financial industry and has been a very important pillar of all options trading since. One of its core assumptions is that the volatility of the underlying asset is constant. It was realised early that one has to specify a dynamic on the volatility itself to get closer to market behaviour. There are mainly two aspects making this fact apparent. Considering historical evolution of volatility by analysing time series data one observes erratic behaviour over time. Secondly, backing out implied volatility from daily traded plain vanilla options, the volatility changes with strike. The most common realisations of this phenomenon are the implied volatility smile or skew. The natural question arises how to extend the Black-Scholes model appropriately. Within this book the concept of stochastic volatility is analysed and discussed with special regard to the numerical problems occurring either in calibrating the model to the market implied volatility surface or in the numerical simulation of the two-dimensional system of stochastic differential equations required to price non-vanilla financial derivatives. We introduce a new stochastic volatility model, the so-called Hyp-Hyp model, and use Watanabe's calculus to find an analytical approximation to the model implied volatility. Further, the class of affine diffusion models, such as Heston, is analysed in view of using the characteristic function and Fourier inversion techniques to value European derivatives.

Információ a könyvről

Angol